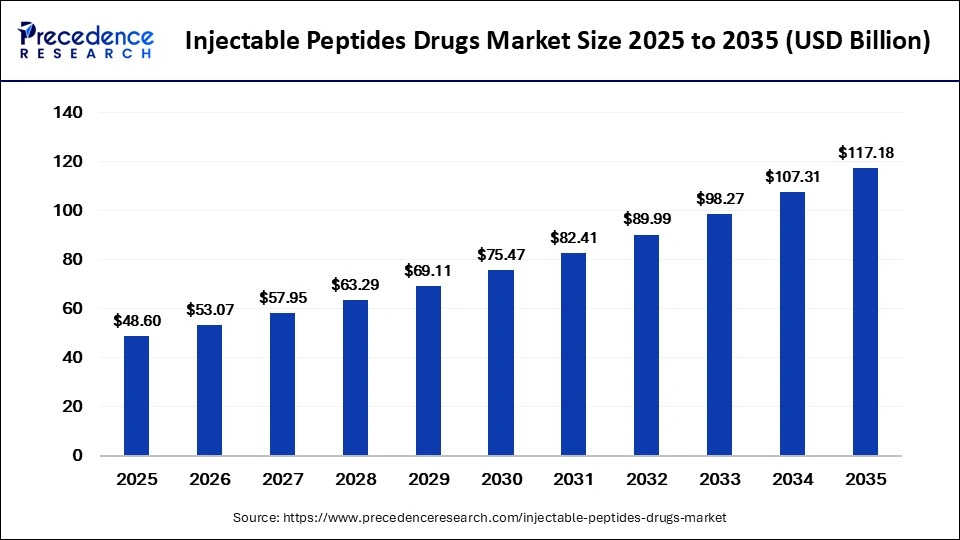

The global injectable peptides drugs market is witnessing rapid expansion as healthcare systems increasingly shift toward targeted and precision-based therapeutics. The market size was valued at USD 48.60 billion in 2025 and is projected to rise from USD 53.07 billion in 2026 to approximately USD 117.18 billion by 2035, registering a CAGR of 9.20% from 2026 to 2035. The growing prevalence of chronic metabolic disorders, rising obesity rates, advancements in peptide engineering, and increasing demand for biologics are among the major factors fueling market growth.

Injectable peptide drugs have emerged as highly effective therapeutic solutions due to their strong receptor specificity, lower toxicity profiles, and improved therapeutic outcomes. These therapies are increasingly being utilized across diabetes management, oncology, cardiovascular care, endocrine disorders, and gastrointestinal diseases. Moreover, innovations in long-acting formulations and self-administered delivery systems are transforming patient adherence and convenience.

Injectable Peptides Drugs Market Key Points

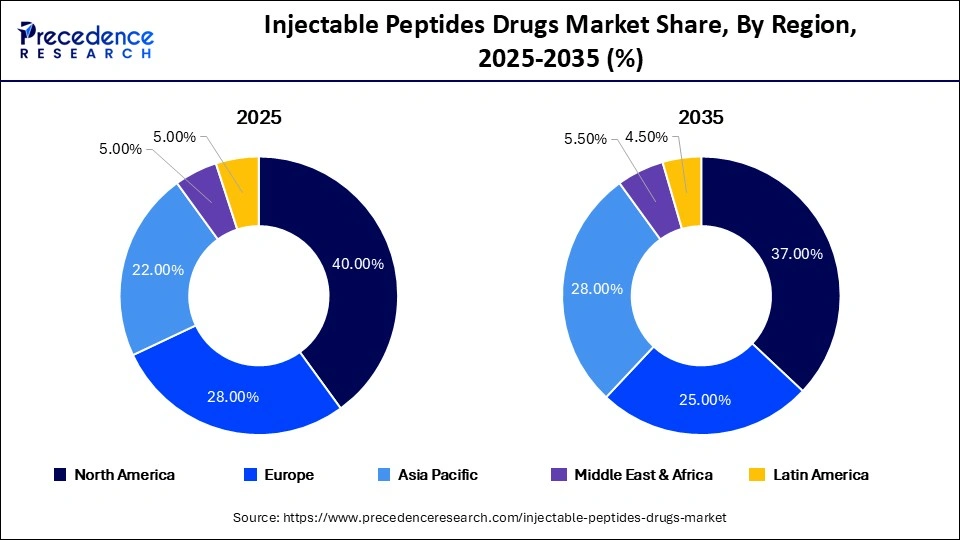

- North America dominated the injectable peptides drugs market in 2025 by accounting for nearly 40% of total market revenue, supported by strong biologics adoption and high healthcare spending.

- Asia Pacific is anticipated to witness the fastest growth during the forecast period with a CAGR of 11.5%, driven by expanding healthcare infrastructure and rising chronic disease prevalence.

- Insulin and insulin analogs remained the leading drug category in 2025 with a 35% market share due to the global rise in diabetes cases.

- GLP-1 receptor agonists emerged as the fastest-growing drug segment and are projected to expand at a CAGR of 14.5% through 2035 because of increasing obesity management applications.

- Diabetes and obesity management represented the largest application segment with a 45% market share in 2025 as metabolic disorders continue to rise globally.

- Subcutaneous injections accounted for 70% of the market in 2025 owing to their convenience for home-based administration and chronic disease treatment.

- Hospital pharmacies led distribution channels with a 45% revenue share due to the need for controlled storage and supervised injectable therapy administration.

- Hospitals and clinics captured 50% of market demand in 2025 because of advanced treatment capabilities and increasing peptide-based oncology procedures.

Why Are Injectable Peptide Drugs Becoming Essential in Modern Therapeutics?

Injectable peptide drugs are rapidly becoming a cornerstone of modern medicine due to their ability to target specific disease pathways while minimizing side effects. Unlike traditional small-molecule drugs, peptides offer higher biological compatibility and superior therapeutic precision. This makes them highly effective for chronic diseases requiring long-term management, including diabetes, obesity, cardiovascular disorders, endocrine diseases, and cancer.

The growing preference for biologics and personalized medicine is also accelerating the adoption of peptide-based therapies. Pharmaceutical companies are investing heavily in next-generation peptide formulations that provide longer activity duration, improved stability, and enhanced patient compliance.

How is Artificial Intelligence Transforming the Injectable Peptides Drugs Market?

Artificial intelligence is revolutionizing the injectable peptides drugs industry by accelerating peptide discovery, molecular optimization, and clinical development. AI-driven systems can rapidly analyze large biological datasets to identify peptide candidates with improved binding affinity, efficacy, and safety profiles. This significantly reduces drug development timelines and lowers research costs.

AI technologies are also improving manufacturing efficiency through predictive analytics, automated quality monitoring, and process optimization. In clinical trials, AI helps improve patient selection, treatment prediction, and outcome analysis, increasing the probability of successful drug approvals. As pharmaceutical firms increasingly integrate AI into biologics development pipelines, the peptide therapeutics market is expected to witness faster innovation cycles.

Injectable Peptides Drugs Market Key Attributes

| Market Indicator | Value |

|---|---|

| Market Size 2025 | USD 48.60 Billion |

| Market Size 2026 | USD 53.07 Billion |

| Forecast Market Size 2035 | USD 117.18 Billion |

| CAGR (2026–2035) | 9.20% |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Leading Application | Diabetes & Obesity Management |

| Leading Route of Administration | Subcutaneous Injection |

What Are the Major Growth Factors Fueling Market Expansion?

Rising Prevalence of Chronic Diseases: The increasing burden of diabetes, obesity, cardiovascular disorders, hormonal imbalances, and cancer is significantly boosting demand for injectable peptide therapies. Aging populations, sedentary lifestyles, and unhealthy dietary patterns continue to increase chronic disease incidence globally.

Rapid Expansion of GLP-1 Therapeutics: GLP-1 receptor agonists have transformed obesity and diabetes management. Their ability to suppress appetite, regulate glucose levels, and support weight loss has created substantial commercial demand worldwide.

Advancements in Peptide Engineering: Innovations in peptide synthesis, purification, stabilization, and conjugation technologies are improving drug efficacy and manufacturability. These advancements are enabling pharmaceutical companies to develop more complex peptide therapeutics.

Growth of Precision Medicine: Personalized healthcare approaches are driving the need for targeted peptide therapies capable of treating disease-specific pathways while minimizing adverse effects.

Increased Biopharmaceutical Investments: Leading pharmaceutical and biotechnology companies are aggressively expanding peptide drug pipelines through partnerships, acquisitions, and R&D investments.

Can Long-Acting Injectable Technologies Unlock New Opportunities?

Long-acting delivery technologies are creating substantial opportunities across the injectable peptides drugs market. Pharmaceutical companies are increasingly focusing on sustained-release systems, biodegradable carriers, depot injections, and advanced delivery devices that reduce dosing frequency and improve treatment adherence.

These technologies are particularly valuable in chronic disease management where patients require long-term treatment. Reduced injection frequency enhances patient convenience while improving therapeutic consistency.

Additionally, oral-to-injectable transition technologies are helping optimize drug bioavailability and efficacy. This trend is expected to reshape the future of peptide therapeutics across metabolic and oncological applications.

Why Are GLP-1 Receptor Agonists Emerging as a Key Revenue Engine?

The GLP-1 receptor agonists segment accounted for 30% of market share in 2025 and is projected to expand at the fastest CAGR of 14.5% through 2035. The explosive growth of obesity management therapies has significantly increased global demand for GLP-1 drugs.

These therapies not only regulate glucose levels but also promote substantial weight reduction and cardiovascular health improvement. Growing awareness regarding obesity-related complications is accelerating adoption among healthcare providers and patients alike.

Pharmaceutical companies are actively competing to launch next-generation GLP-1 therapies with improved efficacy and longer dosing intervals.

Injectable Peptides Drugs Market Segmentation

By Drug Type

The insulin & insulin analogs segment accounted for the largest share of 35% in 2025. Rising cases of type 1 and type 2 diabetes, driven by obesity, sedentary lifestyles, and aging populations, continue to increase demand for insulin therapies. These drugs remain the primary treatment option for effective blood glucose management.

The GLP-1 receptor agonists segment captured 30% of the market in 2025 and is projected to expand at the fastest CAGR of 14.5% through 2035. Increasing adoption for obesity and metabolic disorder treatment is boosting demand. These therapies help regulate blood sugar, suppress appetite, and support weight loss.

The GnRH analogs segment held a 10% market share in 2025. Growth is driven by their extensive use in hormone-dependent cancers such as breast and prostate cancer, along with reproductive health treatments.

Somatostatin analogs represented 10% of the market in 2025. Their role in treating endocrine disorders, acromegaly, carcinoid tumors, and hormone-secreting conditions continues to support segment growth.

Injectable Peptides Drugs Market Share, By Drug Type, 2025-2035 (%)

| Drug Type | 2025 | 2035 | CAGR (%) |

| Insulin & Insulin Analogs | 35.00% | 30.00% | 7.50% |

| GLP-1 Receptor Agonists | 30.00% | 38.00% | 14.50% |

| GnRH Analogs | 10.00% | 9.00% | 7.50% |

| Somatostatin Analogs | 10.00% | 9.00% | 7.00% |

| Parathyroid Hormone Analogs | 5.00% | 5.00% | 8.00% |

| Other Therapeutic Peptides | 10.00% | 9.00% | 8.50% |

By Application

The diabetes & obesity management segment dominated the injectable peptides drugs market with a 45% share in 2025. The rising prevalence of obesity and type 2 diabetes has significantly increased the adoption of peptide-based therapies.

The oncology segment accounted for 15% of the market in 2025 and is expected to grow steadily. Peptide drugs are increasingly used in targeted cancer therapies due to their ability to improve treatment precision and minimize side effects.

The endocrine disorders segment held a 15% share in 2025. Peptide hormones are widely used for thyroid disorders, hormone deficiencies, and other chronic endocrine conditions.

Cardiovascular diseases represented 10% of the market in 2025. Rising incidences of heart disease and cardiometabolic disorders are driving the use of peptide therapies for blood pressure and heart function management.

Injectable Peptides Drugs Market Share, By Application, 2025-2035 (%)

| Application | 2025 | 2035 | CAGR (%) |

| Diabetes & Obesity Management | 45.00% | 50.00% | 11.50% |

| Oncology | 15.00% | 14.00% | 8.00% |

| Endocrine Disorders | 15.00% | 13.00% | 7.50% |

| Cardiovascular Diseases | 10.00% | 9.00% | 8.50% |

| Gastrointestinal Disorders | 10.00% | 8.00% | 7.50% |

| Others | 5.00% | 6.00% | 9.00% |

By Route of Administration

Subcutaneous injection held the largest share of 70% in 2025 due to its convenience and suitability for self-administration. It is widely preferred for chronic conditions such as diabetes and obesity because it supports sustained drug release and reduces hospital visits.

The intravenous injection segment accounted for 20% of the market in 2025. Hospitals continue to rely on IV administration for rapid drug delivery in cancer care and emergency treatments.

Intramuscular injections held a 10% share in 2025. This route is commonly used for long-acting hormone therapies and peptide-based vaccines.

Injectable Peptides Drugs Market Share, By Route of Administration, 2025-2035 (%)

| Route of Administration | 2025 | 2035 | CAGR (%) |

| Subcutaneous Injection | 70.00% | 72.00% | 9.50% |

| Intravenous Injection | 20.00% | 18.00% | 8.00% |

| Intramuscular Injection | 10.00% | 10.00% | 8.50% |

By Distribution Channel

Hospital pharmacies dominated the market with a 45% share in 2025. Injectable peptide drugs often require specialized handling, storage, and professional supervision, making hospitals a key distribution channel.

Retail pharmacies accounted for 35% of the market in 2025. Growth is supported by expanding pharmacy networks and increasing demand for diabetes and obesity treatments.

Online pharmacies held a 20% share in 2025 and are projected to grow rapidly at a CAGR of 13.5%. Rising adoption of telehealth and e-commerce platforms is accelerating online drug sales.

njectable Peptides Drugs Market Share, By Distribution Channel, 2025-2035 (%)

| Distribution Channel | 2025 | 2035 | CAGR (%) |

| Hospital Pharmacies | 45.00% | 42.00% | 8.00% |

| Retail Pharmacies | 35.00% | 33.00% | 9.00% |

| Online Pharmacies | 20.00% | 25.00% | 13.50% |

By End-Use

Hospitals and clinics accounted for 50% of the market share in 2025. These facilities remain the primary centers for administering injectable peptide therapies for cancer, metabolic, and endocrine diseases.

The homecare settings segment represented 30% of the market in 2025 and is expected to grow at the fastest pace. Increasing use of prefilled syringes and auto-injectors is encouraging self-administration at home.

Specialty treatment centers held a 20% market share in 2025. These facilities focus on targeted treatments for cancer, metabolic disorders, and rare endocrine diseases.

Injectable Peptides Drugs Market Share, By End-Use, 2025-2035 (%)

| End-Use | 2025 | 2035 | CAGR (%) |

| Hospitals & Clinics | 50.00% | 47.00% | 8.00% |

| Homecare Settings | 30.00% | 35.00% | 11.50% |

| Specialty Treatment Centers | 20.00% | 18.00% | 8.50% |

By Peptide Type

Long-chain peptides dominated the market with a 40% share in 2025. Their ability to provide sustained drug release and reduce dosing frequency improves patient compliance in chronic disease management.

Modified and conjugated peptides accounted for 35% of the market in 2025 and are projected to grow at the fastest CAGR of 12.5%. Enhanced stability and targeted drug delivery capabilities are driving adoption in oncology and precision medicine.

Short-chain peptides represented 25% of the market in 2025 and continue to be used in several therapeutic applications.

Injectable Peptides Drugs Market Share, By Peptide Type, 2025-2035 (%)

| Peptide Type | 2025 | 2035 | CAGR (%) |

| Long-chain Peptides | 40.00% | 42.00% | 10.50% |

| Modified & Conjugated Peptides | 35.00% | 38.00% | 12.50% |

| Short-chain Peptides | 25.00% | 20.00% | 6.50% |

Injectable Peptides Drugs Market Regional Outlook

North America accounted for 40% of global market revenue in 2025 due to strong biologics adoption, advanced healthcare infrastructure, and high chronic disease prevalence. The region benefits from substantial pharmaceutical R&D spending and the presence of major biotech innovators.

The United States remains the primary growth engine within North America because of increasing demand for GLP-1 therapies, advanced clinical trial capabilities, and growing obesity-related healthcare concerns.

North America Market Forecast

| Region | 2025 Market Size | 2035 Market Size | CAGR |

|---|---|---|---|

| North America | USD 19.44 Billion | USD 47.46 Billion | 9.34% |

| U.S. | USD 14.58 Billion | USD 35.83 Billion | 9.41% |

Asia Pacific is expected to register the highest CAGR of 11.5% through 2035 due to expanding healthcare access, rising disposable income levels, and increasing chronic disease burden across China, India, Japan, and Southeast Asia.

Governments throughout the region are increasing healthcare investments and promoting biologics adoption. The growing middle-class population and rising awareness regarding advanced metabolic therapies are also accelerating demand.

Japan remains a particularly strong market due to its aging population, strong biotechnology ecosystem, and growing focus on precision medicine.

Major Companies Operating in the Injectable Peptides Drugs Market

Novo Nordisk

-

Ozempic (semaglutide): Injectable GLP‑1 receptor agonist for type 2 diabetes (subcutaneous, once‑weekly).

-

Wegovy (higher‑dose semaglutide): GLP‑1‑based injectable for obesity/weight management.

-

Advanced‑stage triple‑agonist UBT‑251 (GLP‑1/GIP/glucagon) in development for obesity.

Eli Lilly

-

Mounjaro (tirzepatide): GLP‑1/GIP dual‑receptor agonist injectable for type 2 diabetes and obesity indications.

-

Retatrutide and other GLP‑1‑based injectables in late‑phase trials for obesity and diabetes.

Amgen

-

MariTide: Investigational once‑monthly injectable peptide for obesity (GLP‑1/GLP‑1R/GLP‑2R‑like multi‑agonist class).

-

Broad biologics pipeline; peptides are an emerging focus in obesity/metabolic area.

Sanofi

-

Not a classical peptide‑injectable leader but has injectable biologics (e.g., monoclonal antibodies) and recently added an injectable, on‑body‑delivered version of Sarclisa (subcutaneous) for blood cancers; not a peptide per se but expands injectable‑portfolio capacity.

-

Engages in large‑scale injectable‑biologics manufacturing under its “Specialty Care” portfolio.

Pfizer

-

Primarily supplies sterile injectables and biosimilar/mAb injectables; not a major branded peptide‑drug marketer yet.

-

Recently entered obesity space via a GLP‑1‑type injectable asset (MET‑097i) with a long‑acting, once‑monthly subcutaneous peptide candidate in development.

Roche (Genentech)

-

CT‑388: Once‑weekly dual GLP‑1/GIP receptor agonist in development as a subcutaneous injectable for obesity and type 2 diabetes.

-

Petrelintide collaboration with Zealand Pharma: injectable amylin‑analog peptide for obesity, to be co‑developed as monotherapy and in fixed‑dose combo with CT‑388.

AstraZeneca

-

Acquired eight long‑acting peptide candidates from CSPC Pharma, including four injectable GLP‑1/GIP‑type peptides for obesity and weight‑related diseases.

-

These are early‑stage injectable peptides; AZ is building an obesity‑focused peptide‑injectable pipeline.

Takeda Pharmaceutical

-

Mainly focused on peptide‑ and biologic‑derived injectables in GI, rare diseases, and oncology (e.g., subcutaneous antibodies and enzyme‑replacement therapies).

-

Has a growing injectable biologics pipeline, but branded peptide‑obesity injectables are less prominent than in Novo/Lilly.

Teva Pharmaceutical

-

Launched the first FDA‑approved generic GLP‑1 injectable for weight loss, supplying a biosimilar‑like peptide‑based subcutaneous product.

-

Also developing long‑acting injectable formulations (e.g., olanzapine LAI) using peptide‑compatible delivery platforms, though not all are peptide‑based drugs per se.

Ipsen

-

Markets Onivyde (irinotecan liposome injection), a nanoliposome‑based injectable used in pancreatic cancer, delivered via IV infusion.

-

Has a broader injectable‑oncology and neurology portfolio; peptide‑centric drugs are secondary to its botulinum toxin and antibody‑based injectables.

Bachem

-

Peptide‑API supplier, not a branded‑drug marketer: produces a wide range of raw and intermediate peptide APIs (hundreds of catalog peptides) for injectable drugs.

-

Focus is on GMP‑grade peptide building blocks for others’ injectable GLP‑1, GLP‑1/GIP, and obesity‑related injectables.

Lonza

-

CDMO for injectable biologics, including monoclonal antibodies and some complex peptides; but Lonza has publicly stated it does not manufacture obesity‑GLP‑1 active peptides themselves.

-

Provides fill‑finish and other injectable‑manufacturing services for originators’ peptide‑based injectables.

CordenPharma

-

Contract manufacturer with a dedicated injectable‑peptide platform, offering clinical and commercial‑scale sterile fill‑finish for injectable peptide drugs.

-

Supports clients developing obesity‑related GLP‑1 and GLP‑1/GIP injectables with end‑to‑end injectable‑product services.

PolyPeptide Group

-

Peptide‑API manufacturer specializing in generic and novel peptide APIs for injectable indications (metabolic, oncology, etc.).

-

Supplies commercial‑scale peptide APIs that feed into other companies’ injectable GLP‑1 and other peptide‑based products.

Zealand Pharma

-

Peptide‑drug developer; owns petrelintide, an amylin‑analog peptide being developed as a subcutaneous injectable for obesity and diabetes.

-

Licensed petrelintide plus combination‑rights to Roche for global co‑development and co‑commercialization of injectable amylin‑ and GLP‑1‑based regimens.

Latest Industry Developments

Eli Lilly Expands Peptide Drug Innovation Pipeline

In February 2026, Eli Lilly entered into a global R&D agreement with Zonsen PepLib Biotech to develop new peptide drug candidates targeting chronic and metabolic diseases.

Manufacturing Expansion in Alabama

In December 2025, Eli Lilly announced investments in a new Alabama-based manufacturing facility focused on peptide and small molecule APIs. The expansion aims to increase production capacity for next-generation anti-obesity and diabetes therapies, including orforglipron.

Segments Covered in the Report

By Drug Type

- GLP-1 Receptor Agonists (Semaglutide, Liraglutide)

- Insulin & Insulin Analogs

- GnRH Analogs

- Somatostatin Analogs

- Parathyroid Hormone (PTH) Analogs

- Other Therapeutic Peptides

By Application

- Diabetes & Obesity Management

- Oncology

- Cardiovascular Diseases

- Endocrine Disorders

- Gastrointestinal Disorders

- Others (Dermatology, Infectious Diseases, etc.)

By Route of Administration

- Subcutaneous Injection

- Intravenous Injection

- Intramuscular Injection

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By End-Use

- Hospitals & Clinics

- Homecare Settings

- Specialty Treatment Centers

By Peptide Type

- Short-chain Peptides

- Long-chain Peptides

- Modified & Conjugated Peptides

By Region

- North America

- Latin America

- Europe

- Asia-pacific

- Middle and East Africa

Read Also: Large-Scale Active Stem Cell Clinical Trials Market Grow at a 14.90% CAGR Through 2035

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @https://www.precedenceresearch.com/sample/8384

You can place an order or ask any questions. Please feel free to contact us at [email protected] |+1 804 441 9344

He is passionate about helping brands grow their digital presence through data-driven marketing strategies and effective content optimization. Akshay continuously follows the latest SEO trends, AI-driven search updates, and performance marketing strategies to deliver sustainable online growth.

Akshay Dhamal is a Digital Marketing Specialist with expertise in SEO, link building, and digital growth strategies. With over two years of experience at Precedence Research, he has hands-on expertise in on-page SEO, off-page SEO, technical SEO, keyword research, and website optimization. He is also a contributing author for Business Web Wire, Market Stats Insight, Chemical Materials Intelligence, US WebWire, ExpressWeb Wire, and Market Stat News, where he shares insights on digital marketing, market trends, and industry developments.

- Injectable Peptides Drugs Market Surges Toward USD 117.18 Billion by 2035 Amid Rising Demand for Precision Therapies - May 8, 2026

- Oculoplastic Surgery Market Size Expected to Reach USD 18.74 Billion by 2035 - May 7, 2026

- In Vivo CAR-T Therapy Market Surges Toward USD 10.84 Billion by 2035 as AI-Driven Immunotherapy Innovation Reshapes Cancer Care - May 7, 2026