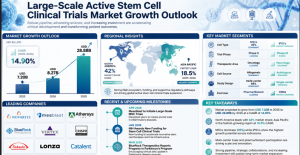

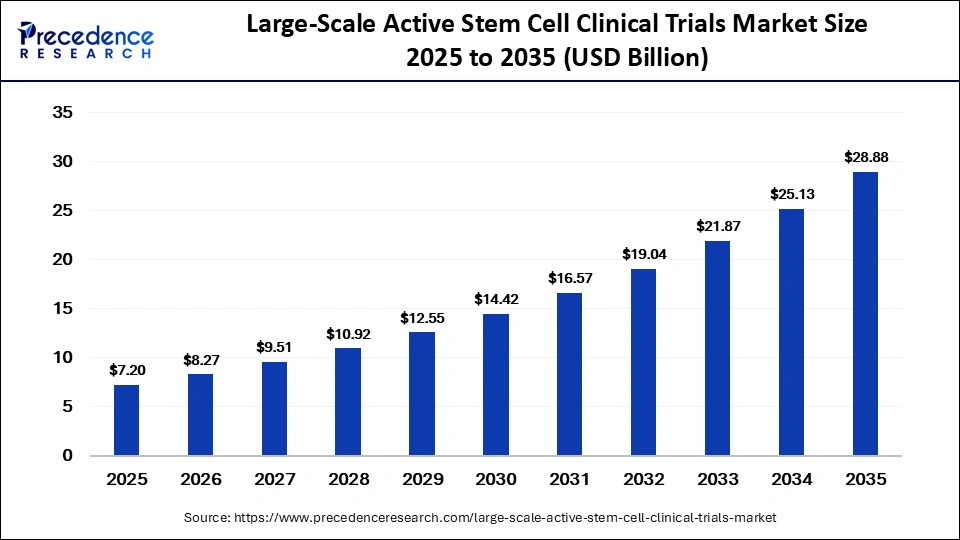

The global large-scale active stem cell clinical trials market is on the rise, with forecasts indicating robust growth from USD 7.20 billion in 2025 to USD 28.88 billion by 2035. With a compound annual growth rate (CAGR) of 14.90% during the forecast period (2026-2035), this market is driven by the increasing demand for regenerative therapies, advancements in stem cell technologies, and the growing application of stem cells in treating chronic and degenerative diseases.

Key drivers behind this growth include expanding clinical trial activities, significant investments in research, and the increasing adoption of stem cell therapies across various medical fields. Stem cells hold great promise in treating a wide range of ailments, including neurological disorders, cardiovascular diseases, and autoimmune conditions. As such, the large-scale stem cell clinical trials market is positioned for continued expansion in the coming years.

Large-Scale Active Stem Cell Clinical Trials Market Key Points

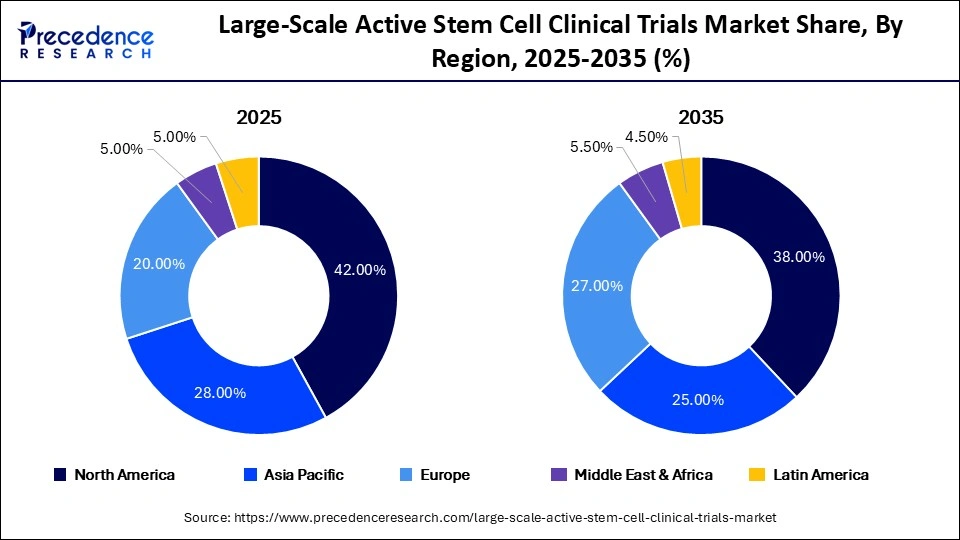

- Top Region in 2025: North America (42% market share)

- Fastest Growing Region: Asia Pacific (CAGR of 18.5% from 2026 to 2035)

- Top Stem Cell Type in 2025: Mesenchymal Stem Cells (MSCs) (35% market share)

- Leading Therapy Type in 2025: Allogeneic Stem Cell Therapies (55% market share)

- Largest Clinical Phase in 2025: Phase II Trials (40% market share)

- Fastest Growing Clinical Phase: Phase III Trials (CAGR of 17.5% from 2026 to 2035)

The Role of AI in the Stem Cell Clinical Trials Market

Artificial Intelligence (AI) is transforming the landscape of stem cell clinical trials. By helping to optimize patient recruitment, predict treatment responses, and improve trial designs, AI is making clinical trials more efficient. AI’s ability to analyze vast datasets quickly provides researchers with insights that can shorten trial timelines and improve accuracy, making it a crucial tool in advancing stem cell therapies.

Furthermore, AI supports more informed decision-making by identifying suitable patient populations and streamlining the process of data analysis. This not only accelerates clinical development but also increases the likelihood of successful outcomes for therapies moving toward commercialization.

Market Growth Factors

The growth of the large-scale active stem cell clinical trials market is being fueled by several key factors:

- Rising Demand for Regenerative Therapies:

Stem cells have become a focal point in regenerative medicine due to their ability to repair or replace damaged tissues. As awareness and acceptance of stem cell therapies increase, clinical trials are expanding to treat a wide array of chronic conditions, thus boosting market activity. - Advancements in Stem Cell Technologies:

Technological advancements in stem cell isolation, processing, and storage are enhancing the efficiency and scalability of clinical trials. These innovations are accelerating the transition of stem cell therapies from early-stage trials to later phases, closer to market adoption. - Supportive Regulatory Environment:

Governments and regulatory bodies around the world are showing strong support for regenerative medicine, providing funding and establishing clear guidelines for clinical trials. This support has fostered a favorable environment for large-scale stem cell trials.

Opportunities and Trends in the Large-Scale Active Stem Cell Clinical Trials Market

The growing demand for personalized medicine is expected to significantly impact the large-scale active stem cell clinical trials market. Stem cell-based treatments, particularly those utilizing autologous therapies (where patients use their own cells), are seen as viable solutions for treating a variety of diseases. As advances are made in the precision of stem cell applications, personalized medicine will continue to open new opportunities for large-scale clinical trials.

Strategic partnerships are accelerating the development and execution of clinical trials. Collaborations between biotech firms, research institutes, and hospitals are enhancing patient recruitment processes, trial design, and clinical outcomes. As these partnerships grow, so does the speed of trial advancements and the efficiency of bringing stem cell therapies to market.

Large-Scale Active Stem Cell Clinical Trials Market Key Attributes

| Report Coverage | Details |

| Market Size in 2025 | USD 7.20 Billion |

| Market Size in 2026 | USD 8.27 Billion |

| Market Size by 2035 | USD 28.88 Billion |

| Market Growth Rate from 2026 to 2035 | CAGR of 14.90% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Stem Cell Type, Clinical Phase, Application, Therapy Type, Trial Design, End-Use, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Large-Scale Active Stem Cell Clinical Trials Market Regional Analysis

North America is expected to maintain its leadership in the large-scale active stem cell clinical trials market, holding 42% of the global market share in 2025. The region benefits from a robust clinical trial infrastructure, substantial funding, and a supportive regulatory environment. This facilitates a high volume of clinical trials, particularly in stem cell-based therapies, driving North America’s dominant position.

Asia Pacific is set to experience the highest CAGR of 18.5% from 2026 to 2035, driven by increasing government support, expanding healthcare infrastructure, and a large patient population. Countries like China and India are emerging as significant players in stem cell trials, providing cost-effective trial operations and attracting international sponsors.

Europe, holding a 28% market share in 2025, is experiencing steady growth in stem cell clinical trials, driven by collaborative research initiatives and advanced healthcare systems. Strong regulatory oversight ensures safety and quality, which enhances the credibility of trials in the region.

Large-Scale Active Stem Cell Clinical Trials Market Segment Analysis

Recent Breakthroughs

- Vertex Pharmaceuticals: On June 20, 2025, Vertex Pharmaceuticals reported a significant breakthrough with positive Phase III results for its stem cell-derived therapy aimed at treating Type 1 diabetes. This progress brings regenerative treatments closer to large-scale commercialization.

- Mesoblast Limited: Mesoblast’s advancement of its allogeneic stem cell therapy into late-stage clinical trials for inflammatory diseases signals strong momentum in the development of scalable cell therapies.

- BlueRock Therapeutics: BlueRock Therapeutics made headlines on March 19, 2026, by progressing its stem cell therapy for Parkinson’s disease to advanced clinical stages. The therapy aims to repair dopaminergic neurons in the brain, offering new hope for those suffering from neurological disorders.

Large-scale Active Stem Cell Clinical Trials Market Key Players

Novartis AG

-

Stem cell‑related offering: Primarily known for CAR‑T cell therapy Kymriah (CTL019), an autologous, ex‑vivo T‑cell therapy, manufactured at its Stein cell‑and‑gene‑therapy facility; this is a gene‑edited lymphocyte product rather than a classic mesenchymal/pluripotent stem‑cell trial, but it is a large‑scale commercial cell‑therapy engine.

-

Large‑scale active trials: Runs and supports multiple global clinical and commercial‑scale programs for Kymriah in hematologic malignancies; these are not “stem cell” trials per se but are high‑volume, GMP‑scale cell‑therapy campaigns.

Fate Therapeutics, Inc.

-

Stem cell‑related offering: Allogeneic, iPSC‑derived CAR‑T and NK‑cell product platforms (e.g., FT819, FT596, FT538, FT576) targeting hematologic and solid tumors; these are investigator‑started and company‑led trials involving large‑scale, off‑the‑shelf iPSC‑derived immune cells.

-

Large‑scale active trials:

-

FT819 Phase 1 basket study in multiple US/UK/EU sites investigating relapsed or refractory B‑cell malignancies and autoimmune indications (lupus nephritis; RMAT‑designated), with plans to move into Phase 2 across indications.

-

Multiple other FT‑platform trials (e.g., FT596, FT576) in Phase 1/2 in leukemias and lymphomas.

-

Mesoblast Limited

-

Stem cell‑related offering: Allogeneic mesenchymal lineage cell therapies from adult bone‑marrow–derived multipotent adult progenitor cells (MAPC), in immunology, neurology, cardiovascular, and orthopedics.

-

Large‑scale active trials:

-

Multiple Phase 2/3 programs across graft‑versus‑host disease (GVHD), heart failure, back‑pain/orthopedic, and inflammatory diseases; several are multi‑site, international trials evaluating immunomodulatory cell products.

-

Athersys, Inc.

-

Stem cell‑related offering: MultiStem (MAPC‑based allogeneic stem cell product) for neurological and critical‑care indications.

-

Large‑scale active trials:

-

MATRICS‑1: Phase 2/3‑style trial in hemorrhagic trauma (targeting 156 patients) using a 3D‑manufactured MultiStem formulation; US‑based, multi‑center, and partially DoD‑funded.

-

MASTERS‑2: Large‑scale Phase 3 trial in ischemic stroke evaluating MultiStem (delivered within 18–48 hours post‑stroke in multiple centers).

-

Pluristem Therapeutics Inc. (now Pluri Inc.)

-

Stem cell‑related offering: Placenta‑derived, allogeneic PLX cells for vascular, hematologic, and inflammatory conditions; the platform is designed for off‑the‑shelf, large‑scale GMP manufacturing.

-

Large‑scale active trials:

-

PLX‑PAD for critical limb ischemia (CLI) and PLX‑RAD for hematologic conditions have advanced to multi‑center Phase 2–3 style trials; clinical‑scale manufacturing is in place to support these campaigns.

-

BlueRock Therapeutics (Bayer AG)

-

Stem cell‑related offering: iPSC‑derived dopaminergic (bemdaneprocel) and photoreceptor (OpCT‑001) cell therapies for Parkinson’s disease and inherited retinal dystrophies.

-

Large‑scale active trials:

-

exPDite‑2 (Phase III): Global, randomized, sham‑surgery‑controlled pivotal trial of bemdaneprocel in Parkinson’s disease; first patients already randomized, marking a true large‑scale, late‑stage stem cell program.

-

CLARICO (Phase 1/2a): First-in‑human iPSC‑derived photoreceptor cell therapy OpCT‑001 for primary photoreceptor diseases (e.g., retinitis pigmentosa), with multi‑site enrollment.

-

Vertex Pharmaceuticals Incorporated

-

Stem cell‑related offering: Stem cell‑derived islet cell therapy (zimislecel / VX‑880, formerly VX‑880) and related encapsulated islet programs for type 1 diabetes.

-

Large‑scale active trials:

-

FORWARD‑101 (Phase 1/2/3 pivotal): Expanded international trial of VX‑880 in patients with T1D and severe hypoglycemia; originally Phase 1/2, now converted to a pivotal Phase 1/2/3 with increased patient numbers (up to 50 subjects) and multi‑country sites.

-

CRISPR Therapeutics AG

-

Stem cell‑related offering: CRISPR‑edited hematopoietic stem cell (HSC) therapies (e.g., exa‑cel/Casgevy for SCD and β‑thalassemia) developed in collaboration with Vertex; also in‑development in vivo HSC‑editing and stem‑cell–derived beta‑cell programs (e.g., CTX211/VCTX210A for T1D).

-

Large‑scale active trials:

-

Casgevy (exa‑cel): Post‑approval, patients are being treated across >50 clinical sites globally for SCD and β‑thalassemia; these are effectively large‑scale, late‑stage cell therapy campaigns even though formally registered as treatment‑access or real‑world‑use settings.

-

CTX211/VCTX210A (PEC‑210A): Phase 1/2 trial of immune‑evasive, stem cell‑derived beta‑cell replacement for T1D, with multi‑site enrollment.

-

Century Therapeutics, Inc.

-

Stem cell‑related offering: iPSC‑derived allogeneic NK and T‑cell therapies (“Allo‑Evasion™” platform) for solid tumors and hematologic malignancies, plus iPSC‑derived beta‑cell programs in autoimmune disease.

-

Large‑scale active trials:

-

CALiPSO‑1 and ELiPSe‑1: Early‑stage but multi‑site clinical programs evaluating iPSC‑derived cell therapies in oncology and autoimmune disease; these are designed from the outset for scalable, large‑scale manufacturing.

-

Lineage Cell Therapeutics, Inc.

-

Stem cell‑related offering: Pluripotent stem cell‑derived differentiated cell products, including OPC1 (oligodendrocyte progenitor cells) for spinal cord injury and OpRegen (retinal pigment epithelium) for geographic atrophy.

-

Large‑scale active trials:

-

DOSED study (OPC1): Phase 1/2a trial in chronic spinal cord injury using a novel delivery device; multi‑site design with plans for expanded enrollment.

-

OpRegen: Phase 1/2a program in age‑related macular degeneration (now partnered with Genentech), with ongoing and planned clinical expansions.

-

Gamida Cell Ltd.

-

Stem cell‑related offering: Nicotinamide‑based ex‑vivo expansion of umbilical cord blood stem cells (NiCord, now mostly branded under omisirge / omidubicel).

-

Large‑scale active trials:

-

NiCord/omidubicel programs: Multi‑center Phase 2/3 trials in hematologic malignancies (e.g., leukemia) using Gamida’s stem‑cell expansion technology; these are large‑scale, transplant‑setting trials across multiple countries.

-

Takeda Pharmaceutical Company Limited

-

Stem cell‑related offering: Historically worked on stem‑cell–based therapies (e.g., Cx611/Cx601 mesenchymal stem cell products for GI indications) via acquisitions such as TiGenix, but these programs are now mostly discontinued or out‑licensed.

-

Large‑scale active trials:

-

As of 2025–2026, Takeda has announced discontinuation of its cell therapy efforts and no current active clinical trials utilizing cell therapy technology; research expertise is being externalized via partnerships.

-

Stemline Therapeutics, Inc. (Menarini Group)

-

Stem cell‑related offering: Primarily focused on small‑molecule and antibody‑based oncology drugs; it does not currently run stem‑cell–based clinical trials.

-

Large‑scale active trials:

-

Active Phase III trials (e.g., ADELA in breast cancer) are immunotherapy‑based but not stem‑cell campaigns; the company’s pipeline is currently non‑cell‑therapy.

-

Lonza Group AG

-

Stem cell‑related offering: A contract development and manufacturing organization (CDMO) providing GMP‑grade iPSC and cell‑therapy manufacturing platforms, including a published clinical‑grade iPSC manufacturing method and master cell banks.

-

Large‑scale active trials:

-

Lonza does not sponsor its own stem cell clinical trials but enables large‑scale active trials of partners’ stem‑cell products (e.g., iPSC‑derived and MSC therapies) via process development, GMP manufacturing, and cell‑banking services.

-

Catalent, Inc.

-

Stem cell‑related offering: CDMO and enabling platform provider with proprietary GMP‑compliant iPSC master cell banks licensed to third‑party developers (e.g., SmartCella) for allogeneic stem‑cell–based therapies.

-

Large‑scale active trials:

-

Catalent does not sponsor stem cell trials itself but supports large‑scale clinical manufacturing of iPSC‑derived and other stem‑cell products through scale‑out facilities and licensed cell‑bank technologies.

-

Segments Covered in the Report

By Stem Cell Type

- Hematopoietic Stem Cells (HSCs)

- Mesenchymal Stem Cells (MSCs)

- Induced Pluripotent Stem Cells (iPSCs)

- Embryonic Stem Cells (ESCs)

By Clinical Phase

- Phase I Trials

- Phase II Trials

- Phase III Trials

By Application

- Oncology

- Cardiovascular Diseases

- Neurological Disorders

- Orthopedic & Musculoskeletal Disorders

- Autoimmune Diseases

- Others (Dermatology, Ophthalmology, etc.)

By Therapy Type

- Autologous Stem Cell Therapies

- Allogeneic Stem Cell Therapies

By Trial Design

- Single-center Trials

- Multi-center Trials (Global Trials)

By End-Use

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations (CROs)

By Region

- North America

- Latin America

- Europe

- Asia-pacific

- Middle and East Africa

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/8379

You can place an order or ask any questions. Please feel free to contact us at [email protected] |+1 804 441 9344

He is passionate about helping brands grow their digital presence through data-driven marketing strategies and effective content optimization. Akshay continuously follows the latest SEO trends, AI-driven search updates, and performance marketing strategies to deliver sustainable online growth.

Akshay Dhamal is a Digital Marketing Specialist with expertise in SEO, link building, and digital growth strategies. With over two years of experience at Precedence Research, he has hands-on expertise in on-page SEO, off-page SEO, technical SEO, keyword research, and website optimization. He is also a contributing author for Business Web Wire, Market Stats Insight, Chemical Materials Intelligence, US WebWire, ExpressWeb Wire, and Market Stat News, where he shares insights on digital marketing, market trends, and industry developments.

- Injectable Peptides Drugs Market Surges Toward USD 117.18 Billion by 2035 Amid Rising Demand for Precision Therapies - May 8, 2026

- Oculoplastic Surgery Market Size Expected to Reach USD 18.74 Billion by 2035 - May 7, 2026

- In Vivo CAR-T Therapy Market Surges Toward USD 10.84 Billion by 2035 as AI-Driven Immunotherapy Innovation Reshapes Cancer Care - May 7, 2026