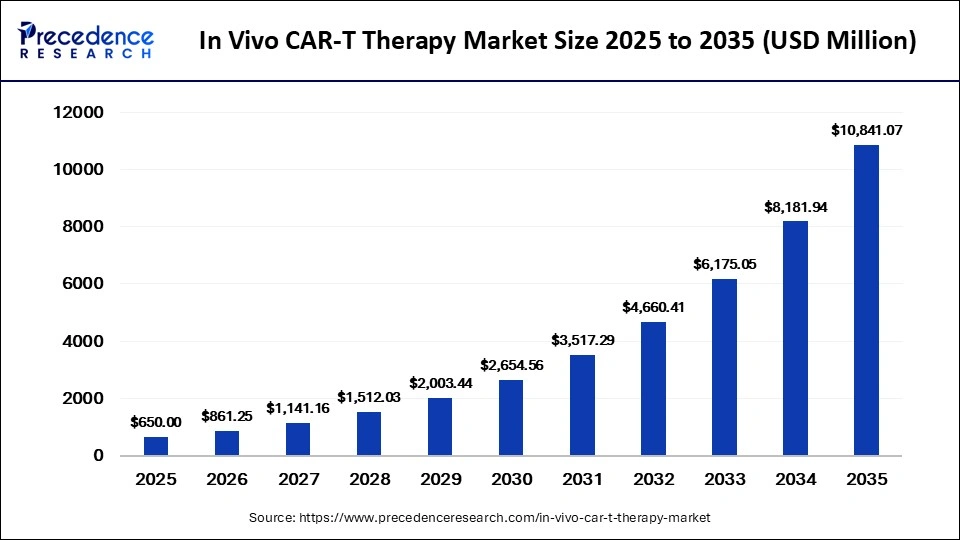

The global in vivo CAR-T therapy market is entering a transformative growth phase, with market size projected to increase from USD 861.25 million in 2026 to approximately USD 10,841.07 million by 2035, expanding at a remarkable CAGR of 32.50% during the forecast period. The market was valued at USD 650 million in 2025 and is witnessing strong momentum due to the growing burden of cancer, increasing clinical trial activity, advancements in gene-editing platforms, and rising confidence in next-generation immunotherapies.

Unlike conventional ex vivo CAR-T therapies that require complex cell extraction and manufacturing procedures, in vivo CAR-T therapy directly reprograms T cells inside the patient’s body using advanced delivery systems such as viral vectors, lipid nanoparticles, and gene-editing technologies. This innovation significantly reduces manufacturing complexity, lowers treatment turnaround time, and opens new possibilities for broader patient accessibility.

The emergence of scalable in vivo platforms is redefining the future of cancer immunotherapy, particularly for patients suffering from relapsed or refractory hematologic malignancies. At the same time, ongoing research into solid tumors and autoimmune diseases is widening the therapeutic scope of this breakthrough technology.

In Vivo CAR-T Therapy Market Key Highlights

- The global in vivo CAR-T therapy market was valued at USD 650 million in 2025 and is forecast to reach USD 10,841.07 million by 2035.

- The market is expected to grow at a robust CAGR of 32.50% between 2026 and 2035.

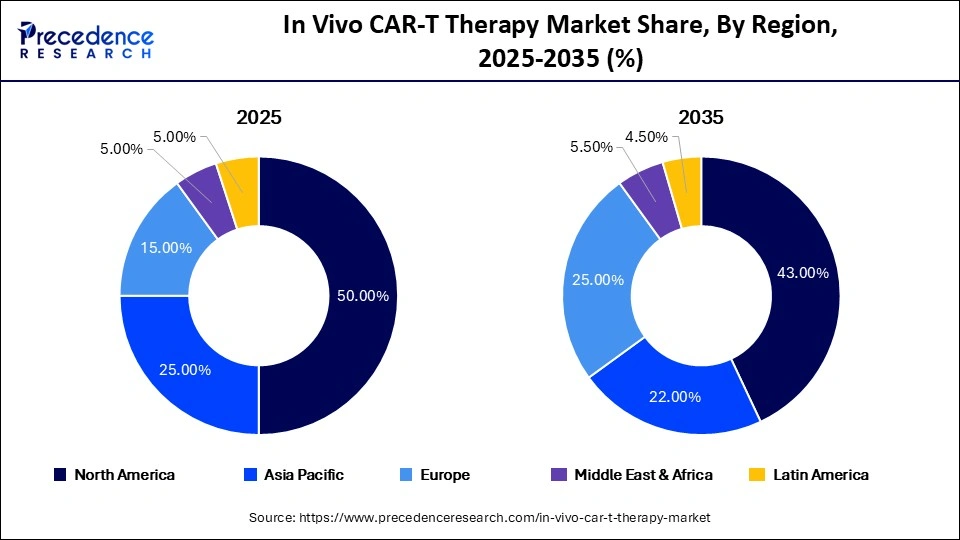

- North America dominated the market in 2025 with a 50% revenue share due to its advanced biotechnology ecosystem and strong clinical pipeline.

- Asia Pacific is projected to emerge as the fastest-growing regional market during the forecast period.

- Viral vector-based platforms accounted for the largest market share of 65% in 2025 owing to established delivery efficiency.

- Non-viral vector-based technologies are expected to witness the fastest growth because of lower immunogenicity and enhanced scalability.

- CD19 remained the leading target antigen segment with a 35% market share in 2025.

- Hematologic malignancies generated the highest application revenue share of 60% in 2025.

- Systemic delivery methods dominated with a 70% market share due to widespread intravenous administration practices.

- Hospitals accounted for the largest end-use segment share of 45% in 2025.

Why Is In Vivo CAR-T Therapy Emerging as the Next Frontier in Oncology?

In vivo CAR-T therapy is rapidly gaining attention as one of the most disruptive innovations in cellular immunotherapy. The technology enables direct genetic modification of immune cells inside the patient’s body without requiring extensive ex vivo cell processing facilities.

Traditional CAR-T therapy involves harvesting T cells from patients, genetically engineering them in specialized laboratories, and reinfusing them into the body. While clinically effective, this process is expensive, time-consuming, and operationally complex. In vivo CAR-T therapy addresses these challenges by delivering CAR constructs directly into the bloodstream using viral and non-viral delivery systems.

This approach offers several advantages, including reduced manufacturing costs, shorter treatment timelines, improved scalability, and potentially wider access across healthcare systems. Researchers are also exploring applications beyond blood cancers, including solid tumors, fibrosis-related diseases, autoimmune disorders, and regenerative medicine.

In Vivo CAR-T Therapy Market Size Snapshot

| Metric | Details |

|---|---|

| Market Size 2025 | USD 650 Million |

| Market Size 2026 | USD 861.25 Million |

| Forecast Market Size 2035 | USD 10,841.07 Million |

| CAGR (2026-2035) | 32.50% |

| Leading Region | North America |

| Fastest Growing Region | Asia Pacific |

How Is Artificial Intelligence Transforming the In Vivo CAR-T Therapy Market?

Artificial intelligence is becoming an essential component in the advancement of in vivo CAR-T therapy development. AI-powered algorithms are helping researchers optimize CAR construct design, predict immune responses, improve vector targeting accuracy, and reduce off-target effects during therapy development.

Machine learning tools are increasingly being utilized to identify novel tumor antigens, analyze tumor microenvironment complexity, and accelerate patient stratification. These technologies are improving the precision and safety profile of next-generation CAR-T therapies.

AI is also streamlining manufacturing workflows and supporting predictive safety modeling. By analyzing massive biological datasets, AI platforms can identify optimal gene delivery systems and forecast therapeutic efficacy more efficiently than traditional approaches.

As biotechnology companies intensify investments in AI-assisted drug development, the convergence of artificial intelligence and immunotherapy is expected to become a major catalyst for future market expansion.

What Are the Major Growth Drivers Accelerating the Market?

Rising Global Cancer Burden and Expanding Clinical Trials

The increasing incidence of leukemia, lymphoma, multiple myeloma, and other cancers continues to drive demand for innovative immunotherapies. The growing number of clinical trials focused on in vivo CAR-T therapy is significantly accelerating market development.

Biotechnology firms and academic institutions are aggressively investing in next-generation CAR-T platforms to improve treatment accessibility and reduce manufacturing barriers associated with conventional therapies.

Rapid Advances in Gene Delivery Technologies

Innovations in lentiviral vectors, lipid nanoparticles (LNPs), circular RNA technologies, CRISPR-based integration systems, and polymeric nanoparticles are improving delivery precision, therapeutic efficacy, and safety outcomes.

These advancements are making in vivo CAR-T therapies increasingly scalable and commercially viable.

Increasing Healthcare Infrastructure and Funding Support

Growing investments in oncology research, biotechnology infrastructure, and precision medicine programs are strengthening the market ecosystem. Governments and private organizations are also increasing funding for advanced cancer therapies and translational research initiatives.

Opportunities Are Emerging in the In Vivo CAR-T Therapy Market

Yes. One of the most significant opportunities lies in the ability of in vivo CAR-T therapy to dramatically reduce manufacturing complexity and operational costs. Traditional CAR-T therapies involve expensive GMP facilities and lengthy cell engineering procedures.

In vivo platforms eliminate several manufacturing stages, enabling faster and more affordable treatment delivery. This could make CAR-T therapy accessible to a much larger patient population globally.

Researchers are increasingly targeting solid tumors such as HER2, EGFR, and mesothelin-positive cancers. Historically, CAR-T therapies faced biological limitations in solid tumor environments. However, next-generation receptor engineering and advanced targeting mechanisms are overcoming these barriers.

As clinical success in solid tumors improves, the market is expected to unlock substantial new growth opportunities.

In Vivo CAR-T Therapy Market Major Trends

The industry is witnessing rapid innovation in mRNA lipid nanoparticles, viral vectors, CRISPR technologies, and nanoparticle-mediated gene delivery systems. These technologies are improving targeting accuracy while minimizing systemic toxicity.

Third-generation CAR-T cells incorporating multiple signaling domains are enhancing immune persistence, therapeutic durability, and tumor-killing efficiency.

Emerging therapies such as GT-801 are advancing the landscape through lipid nanoparticle-mediated mRNA delivery approaches that enable direct T-cell programming inside the body.

In Vivo CAR-T Therapy Market Segment Analysis

Vector Type Insights

The viral vector-based segment accounted for the largest market share of 65% in 2025. Viral vectors such as lentiviral and AAV systems have demonstrated high gene delivery efficiency and strong clinical performance in early-stage studies.

These platforms continue to dominate due to their established reliability and robust transduction capabilities.

| Vector Type | 2025 Share | 2035 Share | CAGR |

|---|---|---|---|

| Viral Vector-based | 65% | 55% | 28.0% |

| Non-Viral Vector-based | 35% | 45% | 38.5% |

However, non-viral technologies are expected to witness the fastest expansion owing to improved scalability, lower immunogenicity, and enhanced design flexibility.

Target Antigen Insights

The CD19 segment captured 35% market share in 2025 because of its proven success in B-cell malignancy treatment. CD19 remains one of the most validated and clinically successful targets in CAR-T therapy.

Meanwhile, solid tumor targets are expected to grow at the fastest CAGR due to increasing research into HER2, EGFR, mesothelin, and other tumor-specific antigens.

| Target Antigen | 2025 Share | 2035 Share | CAGR |

|---|---|---|---|

| CD19 | 35% | 30% | 26.5% |

| BCMA | 25% | 28% | 32.5% |

| Solid Tumor Targets | 25% | 30% | 40.0% |

| CD20 | 15% | 12% | 25.0% |

Application Insights

Hematologic malignancies accounted for 60% of market revenue in 2025 due to the demonstrated clinical effectiveness of CAR-T therapies in leukemia, lymphoma, and multiple myeloma treatment.

At the same time, solid tumors are emerging as the fastest-growing application segment due to significant unmet medical needs and ongoing technological improvements.

| Application | 2025 Share | 2035 Share | CAGR |

|---|---|---|---|

| Hematologic Malignancies | 60% | 50% | 28.0% |

| Solid Tumors | 25% | 35% | 40.5% |

| Autoimmune Diseases | 15% | 15% | 30.0% |

Delivery Method Insights

Systemic intravenous delivery held 70% market share in 2025 due to its ease of administration and compatibility with existing hospital infrastructure.

However, localized delivery approaches are gaining traction because they improve tumor targeting while minimizing systemic exposure and toxicity.

| Delivery Method | 2025 Share | 2035 Share | CAGR |

|---|---|---|---|

| Systemic Delivery | 70% | 65% | 30.0% |

| Localized Delivery | 30% | 35% | 36.5% |

End-Use Insights

Hospitals Lead the Market with 45% Share in 2025

In 2025, hospitals dominated the in vivo CAR-T therapy market, holding a 45% share. Their comprehensive infrastructure supports a wide range of services, including diagnostics, consultations, and specialized treatments, making them the preferred choice for patients requiring advanced therapy.

Market Share by End-Use (2025-2035)

- Hospitals: 45% in 2025, expected to decrease to 42% by 2035, with a CAGR of 29%.

- Specialized Cancer Centers: 40% in 2025, projected to grow at the fastest CAGR of 34%, reaching 43% by 2035.

- Academic & Research Institutes: 15% in 2025, expected to remain steady, with a CAGR of 28%.

Specialized cancer centers are anticipated to grow rapidly due to their expert focus on advanced therapies and continued infrastructure investments. Academic and research institutes, essential for early-stage clinical trials, play a key role in innovation and provide patients with early access to groundbreaking treatments.

In Vivo CAR-T Therapy Market Regional Outlook

North America dominated the global market with a 50% share in 2025 due to strong biotechnology innovation, a highly active clinical trial ecosystem, advanced healthcare infrastructure, and significant research funding.

The United States remains the key growth engine owing to FDA support, robust reimbursement frameworks, and the presence of leading biotechnology companies.

| Region | 2025 Share |

|---|---|

| North America | 50% |

| Europe | 25% |

| Asia Pacific | 15% |

Europe remains the second-largest market due to strong academic collaborations and regulatory advancements.

Asia Pacific is expected to witness the fastest growth, driven by increasing clinical research activity, expanding biotech investments, and supportive government initiatives across China, Japan, and South Korea.

Competitive Landscape: Leading Companies in the In Vivo CAR-T Therapy Market

-

Capstan Therapeutics: Lead offering CPTX2309 (anti-CD19 LNP-mRNA); targets autoimmune diseases via B-cell depletion; Phase 1 initiated; $2.1B AbbVie deal.

-

Interius BioTherapeutics: INT2104 (anti-CD20 lentiviral); for B-cell malignancies; Phase 1 dosed first patient; acquired by Gilead/Kite for $350M.

-

Umoja Biopharma: UB-VV111 and UB-VV400 (VivoVec lentiviral, CD19+); B-cell malignancies without lymphodepletion; Phase 1; AbbVie $1.44B opt-in.

-

Sana Biotechnology: SG293 (CD19 fusogen); oncology/autoimmune, CD8+ T cells, liver-sparing; preclinical data presented.

-

Legend Biotech: Active in vivo CAR-T R&D; hiring scientists for life-threatening diseases program.

-

Bristol Myers Squibb: Acquired Orbital ($1.5B); preclinical OTX-201 (anti-CD19) for autoimmune B cells.

-

Gilead Sciences (Kite Pharma): Owns Interius INT2104 (Phase 1); $1.64B Pregene deal for next-gen in vivo CAR-Ts.

-

Novartis AG: Vyriad collaboration on lentiviral in vivo CAR-T; evaluating, no proprietary clinical lead.

-

Others (Ex Vivo Focus/No Clear In Vivo): Cellectis (smart ex vivo CAR-T); Beam (BEAM-201 ex vivo, some HSC editing); Precision (pivoted early CAR-T); Poseida (allogeneic CAR-T); CRISPR (enables research, ex vivo focus); Intellia (CRISPR off-shelf ex vivo); Caribou (vispa-cel ex vivo).

Latest Industry Developments

Gilead’s Kite Pharma Expands Focus on In Vivo CAR-T

In April 2026, Kite Pharma announced strategic plans to expand its in vivo CAR-T pipeline while preparing for a next-generation multiple myeloma cell therapy launch. The company aims to simplify manufacturing and broaden patient accessibility through innovative in vivo technologies.

Eli Lilly Acquires Kelonia Therapeutics

In April 2026, Eli Lilly and Company announced the acquisition of Kelonia Therapeutics, a biotechnology company specializing in in vivo gene delivery systems. Kelonia’s proprietary iGPS platform enables selective T-cell targeting inside the body for CAR-T therapy generation.

These developments highlight growing industry confidence in scalable in vivo immunotherapy platforms.

Segments Covered in the Report

By Vector Type

- Viral Vector-based In Vivo CAR-T (AAV, Lentiviral)

- Non-Viral Vector-based In Vivo CAR-T (LNPs, Electroporation, Nanoparticles)

By Target Antigen

- CD19

- BCMA

- CD20

- Solid Tumor Targets (HER2, EGFR, Mesothelin, etc.)

By Application

- Hematologic Malignancies (Leukemia, Lymphoma, Myeloma)

- Solid Tumors

- Autoimmune Diseases

By Delivery Method

- Systemic Delivery (Intravenous)

- Localized Delivery (Intratumoral, Targeted Delivery)

By End-Use

- Hospitals

- Specialized Cancer Treatment Centers

- Academic & Research Institutes

By Development Stage

- Preclinical Stage

- Clinical Stage (Phase I/II/III)

- Commercialized Therapies

By Region

- North America

- Latin America

- Europe

- Asia-pacific

- Middle and East Africa

Read Also: CAR-T Therapies for Blood Cancers Market Size Projected to Reach USD 38.40 Billion by 2035

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/8380

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344