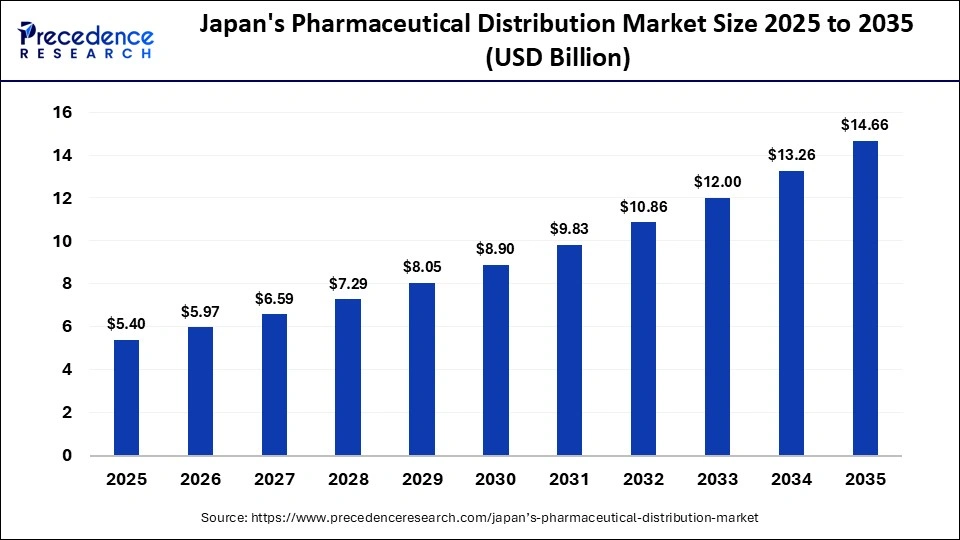

The Japan’s pharmaceutical distribution market is witnessing strong growth, supported by rising demand for prescription drugs, rapid advancements in logistics infrastructure, and the country’s aging population. The market size was valued at USD 5.40 billion in 2025 and is expected to grow from USD 5.97 billion in 2026 to approximately USD 14.66 billion by 2035, expanding at a CAGR of 10.50% during the forecast period.

Pharmaceutical distribution in Japan involves the storage, transportation, and delivery of medicines from manufacturers to hospitals, clinics, and retail pharmacies. The system ensures the timely and safe supply of prescription drugs, biologics, and specialty medications, making it a critical component of the healthcare ecosystem.

Read Also: Ocular Hypertension Market

Key Market Highlights

- Market size expected to reach USD 5.97 billion in 2026

- Forecast to hit USD 14.66 billion by 2035

- Growing at a CAGR of 10.50% (2026–2035)

- Transportation & logistics segment dominated with 28% share in 2025

- Full-line wholesaling led distribution model with 34% share

- Prescription drugs accounted for 70% of total market share

- Hospitals were the leading end-user with 45% share

Market Trends

Expansion of Cold Chain Logistics

The increasing demand for biologics, vaccines, and temperature-sensitive drugs is driving investments in advanced cold chain logistics. Temperature-controlled storage and transportation systems are becoming essential for maintaining drug efficacy.

Growing Aging Population

Japan’s aging demographic is significantly boosting the demand for pharmaceuticals, especially for chronic disease management. This trend is a major contributor to the expansion of distribution networks.

Supply Chain Digitalization

Companies are adopting advanced technologies such as AI, IoT, and automated warehouse systems to enhance inventory management, optimize routes, and improve delivery timelines.

Rise of Specialty and Personalized Medicines

The increasing use of specialty drugs and personalized treatments is creating demand for more sophisticated distribution systems with specialized handling requirements.

Direct-to-Pharmacy and Last-Mile Delivery

Manufacturers are increasingly adopting direct distribution models to improve delivery speed, reduce costs, and enhance supply chain transparency.

Impact of Artificial Intelligence on the Market

Artificial intelligence is playing a transformative role in Japan’s pharmaceutical distribution sector. AI-driven systems analyze real-time data to optimize inventory levels, improve route planning, and enhance warehouse efficiency.

Additionally, AI supports regulatory compliance, quality control, and predictive analytics, enabling distributors to minimize delays and ensure consistent drug availability. These innovations are significantly improving the reliability and efficiency of the pharmaceutical supply chain.

Market Dynamics

Driver: Rising Demand for Prescription Drugs and Aging Population

Japan’s rapidly aging population and increasing prevalence of chronic diseases are driving demand for prescription medications. This, in turn, is boosting the need for efficient pharmaceutical distribution systems.

Restraint: Regulatory Pressure and High Operational Costs

Strict government regulations, controlled drug pricing under the national healthcare system, and high costs associated with cold chain logistics are key challenges for market players.

Opportunity: Digital Supply Chain and Cold Chain Investments

Opportunities lie in expanding cold chain infrastructure, adopting automated logistics systems, and enhancing last-mile delivery services. The growing demand for biologics and personalized medicines further supports market expansion.

Segment Insights

By Service Type

The transportation & logistics segment dominated the market in 2025 with a 28% share, driven by the continuous movement of pharmaceuticals across healthcare facilities. Efficient logistics networks are essential to maintain uninterrupted drug supply.

Cold chain management is expected to witness the fastest growth due to increasing demand for temperature-sensitive drugs such as vaccines and biologics. Storage & warehousing and inventory management also play crucial roles in ensuring availability and reducing stockouts.

By Distribution Model

Full-line wholesaling led the market with a 34% share, supported by its ability to provide a wide range of pharmaceutical products through a single distribution channel.

Third-party logistics (3PL) is emerging as a fast-growing segment, as companies increasingly outsource logistics operations to improve efficiency and reduce costs. Direct-to-pharmacy and direct-to-hospital models are also gaining traction due to faster delivery and improved transparency.

By Product Type

Prescription drugs dominated the market with a 70% share in 2025, driven by increasing chronic diseases and strict regulatory requirements for controlled drug distribution.

Over-the-counter (OTC) drugs accounted for the remaining share, supported by rising self-medication trends and expanding retail pharmacy networks.

By End User

Hospitals held the largest share of 45% in 2025, due to high demand for medications in inpatient and outpatient care.

Retail pharmacies are the second-largest segment and are expected to grow significantly, driven by consumer preference for easy access to medicines. Clinics also contribute steadily as primary healthcare providers.

Government Support and Regulatory Landscape

The Japanese government plays a vital role in supporting the pharmaceutical distribution market through initiatives focused on digitalization, cold chain infrastructure, and ensuring stable drug supply.

Policies from the Ministry of Health, Labour and Welfare aim to improve inventory management and reduce drug shortages. Additionally, strict pricing regulations under the National Health Insurance system ensure affordability while maintaining supply chain stability.

Competitive Landscape

The market is highly competitive, with leading companies focusing on expanding logistics networks, enhancing cold chain capabilities, and adopting advanced technologies. Key players include:

- Medipal Holdings

- Alfresa Holdings Corporation

- Suzuken Co., Ltd.

- Toho Holdings Co., Ltd.

- Nippon Express Holdings

- DHL Supply Chain

- UPS Healthcare

- Kuehne + Nagel

- McKesson Corporation

- Cardinal Health

These companies are investing in automation, digital supply chains, and last-mile delivery solutions to strengthen their market position.

Recent Developments

- In February 2026, Mitsubishi Logistics, Takeda Pharmaceutical, and JR Freight launched temperature-controlled rail containers for pharmaceutical transport.

- In January 2026, Otsuka Pharmaceutical partnered with Towa Pharmaceutical to ensure stable drug supply through collaborative manufacturing systems.

- Companies are increasingly adopting AI-enabled tracking and monitoring systems for temperature-sensitive shipments.

Conclusion

The Japan pharmaceutical distribution market is set for robust growth, driven by demographic shifts, increasing pharmaceutical demand, and advancements in logistics technology. The integration of AI, expansion of cold chain infrastructure, and adoption of digital supply chain systems are reshaping the industry.

As demand for specialty drugs and biologics continues to rise, efficient distribution systems will remain essential in ensuring timely access to medicines, positioning the market for sustained long-term growth.

Get Sample Link: https://www.precedenceresearch.com/sample/8284

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at [email protected]