The implantable sensor orthopedic market is gaining momentum as healthcare providers increasingly adopt smart implants capable of monitoring patient outcomes in real time. Advances in sensor technologies, wireless communication, and AI-driven analytics are expected to transform orthopedic care and create significant opportunities through 2035.

According to Precedence Research, the global implantable sensor orthopedic market size accounted for USD 1.06 billion in 2025 and is predicted to increase from USD 3.06 billion in 2026 to approximately USD 13.17 billion by 2035, expanding at a CAGR of 17.04% from 2026 to 2035. The increasing incidence of accidents and chronic diseases, along with further advancements in healthcare devices, support market growth.

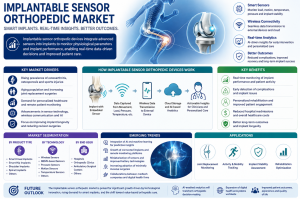

Market Overview

The implantable sensor orthopedic market represents a rapidly evolving segment of orthopedic healthcare, combining implant technologies with advanced sensing capabilities to provide continuous monitoring of physiological parameters and implant performance. These smart devices are designed to improve patient outcomes, optimize rehabilitation, and enable data-driven clinical decisions.

Growing demand for personalized healthcare and the increasing number of joint replacement procedures are accelerating the adoption of implantable sensor technologies. Orthopedic surgeons and healthcare systems are seeking solutions that can provide real-time insights into implant stability, load distribution, temperature changes, and patient mobility. These capabilities help identify complications at an early stage and improve long-term treatment success.

The rising prevalence of osteoarthritis, osteoporosis, sports injuries, and age-related musculoskeletal disorders is contributing to strong market expansion. Aging populations across developed and emerging economies are increasing the need for advanced orthopedic implants that offer enhanced functionality and better patient monitoring.

Technological advancements in microelectronics, biosensors, wireless connectivity, and battery systems are enabling the development of next-generation smart orthopedic implants. Manufacturers are focusing on creating compact, biocompatible, and energy-efficient sensors capable of delivering accurate and continuous data without compromising patient comfort.

Although the market offers substantial opportunities, challenges such as high development costs, regulatory requirements, cybersecurity concerns, and integration with digital health ecosystems remain key considerations. Continued innovation and collaboration between medical device companies and digital health providers are expected to drive long-term growth.

AI Impact

Artificial intelligence is becoming an essential component of implantable sensor orthopedic technologies. AI algorithms can analyze continuous streams of data generated by smart implants, enabling clinicians to identify abnormal patterns and predict potential complications before symptoms become severe.

Machine learning models are supporting personalized rehabilitation by assessing patient mobility, activity levels, and implant performance. These insights help physicians customize treatment plans and improve recovery outcomes following orthopedic surgeries.

AI-powered predictive analytics are also improving preventive care. Data collected from implantable sensors can be used to forecast implant failures, detect infections, and evaluate stress patterns, allowing healthcare providers to intervene earlier and reduce revision surgeries.

Integration of AI with cloud platforms and remote patient monitoring systems is creating new possibilities for connected orthopedic care. As digital health ecosystems continue to evolve, AI-enabled implant technologies are expected to play a major role in the future of orthopedic medicine.

Market Trends

- Growing adoption of smart orthopedic implants with embedded sensors.

- Rising demand for remote patient monitoring technologies.

- Increasing use of AI and predictive analytics in orthopedic care.

- Expansion of wireless communication and cloud-connected implants.

- Strong focus on personalized rehabilitation programs.

- Development of miniaturized and energy-efficient biosensors.

- Increasing investments in digital health and connected medical devices.

- Growing prevalence of osteoarthritis and age-related joint disorders.

- Rising use of minimally invasive orthopedic procedures.

- Strategic collaborations between orthopedic manufacturers and healthcare technology companies.

Market Scope

| Report Coverage | Details |

| Market Size in 2025 | USD 1.06 Billion |

| Market Size in 2026 | USD 3.06 Billion |

| Market Size by 2035 | USD 13.17 Billion |

| Market Growth Rate from 2026 to 2035 | CAGR of 17.04% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Paicfic |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Product Type, Sensor Type, Technology, Application, End User, Distribution Channel, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Segment Insights

By Product Type

Smart knee implants account for a significant share of the market due to the high number of knee replacement procedures performed globally. Implantable sensors help monitor load distribution and patient movement, improving postoperative outcomes.

Smart hip implants are witnessing rapid growth as healthcare providers increasingly adopt technologies that support continuous monitoring and early detection of complications. Shoulder and spinal implants are also emerging as promising areas for sensor integration.

By Technology

Wireless sensor technologies dominate the market because they enable real-time transmission of patient data to clinicians and healthcare systems. Advancements in Bluetooth, radiofrequency communication, and cloud connectivity are enhancing the capabilities of these systems.

MEMS-based sensors are gaining popularity owing to their small size, energy efficiency, and ability to provide precise measurements. These technologies are enabling the development of more sophisticated orthopedic implants.

By End User

Hospitals represent the largest end-user segment due to the increasing number of orthopedic surgeries and the availability of advanced healthcare infrastructure. Specialty orthopedic centers are also witnessing rapid adoption as they focus on improving patient outcomes and reducing revision procedures.

Regional Insights

North America dominates the implantable sensor orthopedic market due to strong healthcare infrastructure, high adoption of advanced medical technologies, and increasing orthopedic procedures. The United States remains a key center for innovation in smart implant technologies.

")

Europe holds a substantial share of the market, supported by increasing investments in digital healthcare and growing demand for minimally invasive orthopedic solutions. Germany, the United Kingdom, and France are leading contributors to regional growth.

Asia-Pacific is expected to witness the fastest growth during the forecast period. Rising healthcare expenditure, expanding elderly populations, and increasing access to advanced orthopedic treatments are supporting market expansion across China, Japan, South Korea, and India.

Latin America is experiencing gradual growth owing to improving healthcare infrastructure and rising awareness regarding advanced orthopedic treatments. Brazil and Mexico remain important markets within the region.

The Middle East and Africa region is showing steady development as governments invest in healthcare modernization and specialized orthopedic care services. Growing medical tourism is also contributing to market growth.

Competitive Landscape

The implantable sensor orthopedic market is characterized by continuous technological innovation and strategic collaborations. Companies are investing heavily in sensor miniaturization, wireless connectivity, and AI-powered analytics to differentiate their product portfolios.

Partnerships between orthopedic implant manufacturers, software companies, and healthcare providers are accelerating the commercialization of smart implant technologies. These collaborations are helping organizations integrate remote monitoring capabilities and digital health platforms.

Leading players are expanding their research activities to develop next-generation implants capable of delivering more precise and actionable data. Product innovation and regulatory approvals are becoming important competitive factors in the market.

As value-based healthcare models gain momentum, manufacturers are increasingly focusing on technologies that improve patient outcomes, reduce hospital readmissions, and minimize revision surgeries.

Leading Key Players in the Market

- Zimmer Biomet Holdings, Inc.

- Stryker Corporation

- Smith+Nephew plc

- Medtronic plc

- Johnson & Johnson (DePuy Synthes)

- Exactech, Inc.

- OrthAlign, Inc.

- Canary Medical Inc.

- Monogram Technologies Inc.

- Conformis, Inc.

- B. Braun SE

- Arthrex, Inc.

- NuVasive, Inc.

- Globus Medical, Inc.

- MicroPort Orthopedics Inc.

Get Sample Link : https://www.precedenceresearch.com/sample/8499

Recent Developments

- In June 2026, Auxano Medical, a company focused on advancing osseointegration and bone-implant interface technology, announced the launch of its newly redesigned website. The updated platform offers surgeons, distributors, and industry partners expanded access to information on Auxano Medical’s proprietary surface morphology technology and its growing portfolio of orthopedic implant systems, including the ARKEO™ Wedge Fixation System and the INTREPED Intraosseous Fusion Device.

- In May 2026, Ortho Development Corporation (ODEV), a designer and manufacturer of high-quality orthopedic implants and surgical instruments, launched the full commercial launch of the Trivicta Hip Stem, a cementless triple-taper femoral component for primary total hip arthroplasty. Following a controlled market introduction, the system is now available to surgeons and health systems nationwide through Ortho Development’s authorized U.S. distribution network.

Segments Covered in the Report

By Product Type

- Smart Knee Implants

- Smart Hip Implants

- Smart Spinal Implants

- Trauma & Extremity Implants

- Others

By Sensor Type

- Pressure Sensors

- Load & Strain Sensors

- Motion Sensors

- Temperature Sensors

- Multi-parameter Sensors

By Technology

- Wireless Sensor-enabled Implants

- Bluetooth-enabled Implants

- IoT-enabled Smart Implants

- AI-integrated Monitoring Implants

By Application

- Joint Replacement Monitoring

- Post-operative Recovery Monitoring

- Rehabilitation & Mobility Tracking

- Infection Detection

- Implant Performance Monitoring

- Others

By End User

- Hospitals

- Orthopedic Specialty Clinics

- Ambulatory Surgical Centers (ASCs)

- Research Institutes & Academic Centers

- Others

By Distribution Channel

- Direct Sales

- Medical Device Distributors

- Group Purchasing Organizations (GPOs)

- Tender Procurement

By Region

- North America

- Latin America

- Europe

- Asia-pacific

- Middle and East Africa

Also Read Our Latest Article : Health and Wellness Market

- Pharmacy Market Size to Surpass USD 1.99 Trillion by 2035 - July 9, 2026

- Bromelain Market Size to Attain USD 66.25 Billion by 2035 - July 9, 2026

- Biotechnology Instruments Market Size to Attain USD 133.49 Bn by 2035 - July 9, 2026