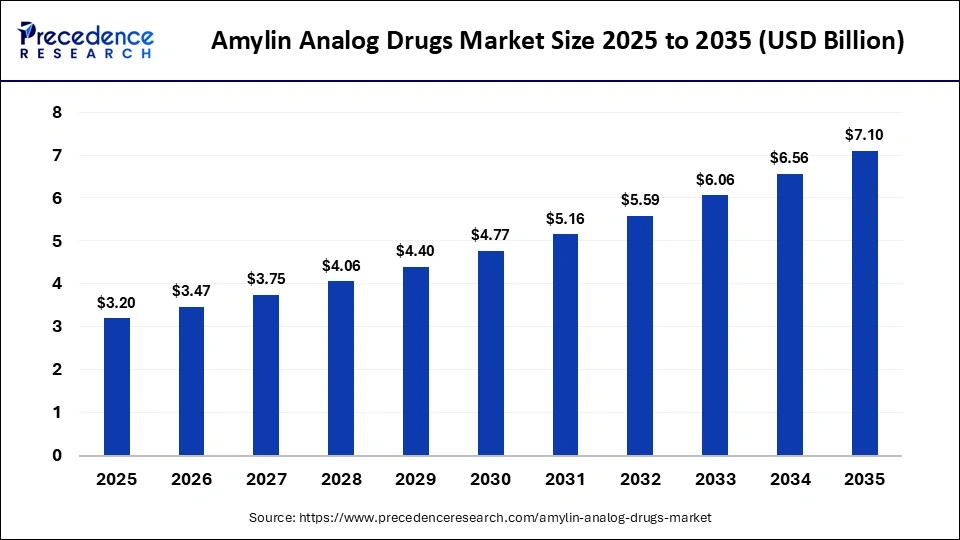

The global amylin analog drugs market size was valued at USD 3.20 billion in 2025 and is projected to increase from USD 3.47 billion in 2026 to approximately USD 7.10 billion by 2035, expanding at a CAGR of 8.30% during the forecast period. The market is gaining traction because of the increasing burden of obesity, type 1 diabetes, and type 2 diabetes across the world. Amylin analog drugs are increasingly being used to improve glycemic control, reduce glucagon secretion, slow gastric emptying, and promote satiety among patients with metabolic disorders.

The market is also benefiting from the rapid evolution of obesity treatments and the growing popularity of combination metabolic therapies. Pharmaceutical companies are investing heavily in long-acting amylin analogs, once-weekly injectables, and dual hormone therapies that combine amylin analogs with GLP-1 receptor agonists. These therapies are showing promising outcomes in weight loss and metabolic control, making them increasingly attractive for both diabetes and obesity management.

Read Also: Day Case Surgery Market

Quick Insights

- The amylin analog drugs market was valued at USD 3.20 billion in 2025 and is expected to reach USD 7.10 billion by 2035.

- The market is forecast to grow at a CAGR of 8.30% between 2026 and 2035.

- North America dominated the market with a 40% share in 2025.

- Asia Pacific is expected to witness the fastest growth, expanding at a CAGR of 9.5% during the forecast period.

- Pramlintide held the leading product share of 55% in 2025.

- Subcutaneous injection accounted for 80% of the market in 2025.

- Type 1 diabetes represented the largest application segment with a 50% share in 2025.

- Hospitals accounted for 60% of the market in 2025.

Amylin Analog Drugs Market Revenue Snapshot

| Metric | Value |

|---|---|

| Market Size in 2025 | USD 3.20 Billion |

| Market Size in 2026 | USD 3.47 Billion |

| Forecast Market Size in 2035 | USD 7.10 Billion |

| CAGR (2026-2035) | 8.30% |

| Largest Regional Market | North America |

| Fastest Growing Region | Asia Pacific |

How Is Artificial Intelligence Influencing the Amylin Analog Drugs Market?

Artificial intelligence is becoming increasingly important in the amylin analog drugs market because it is helping researchers speed up drug discovery, improve clinical trial efficiency, and optimize patient monitoring. AI tools can identify molecular patterns, predict patient responses, and accelerate the development of next-generation amylin analogs with longer duration and fewer side effects.

AI is also supporting remote patient care by improving glucose monitoring, adherence tracking, and dose optimization. Healthcare providers are increasingly using AI-powered platforms to monitor patient outcomes, predict weight changes, and personalize therapy for individuals receiving amylin analog drugs. This trend is expected to strengthen as telemedicine and digital health solutions continue to grow.

What Are the Major Growth Drivers Supporting the Amylin Analog Drugs Market?

One of the biggest growth drivers is the increasing prevalence of obesity and diabetes worldwide. Poor dietary habits, sedentary lifestyles, and aging populations are leading to a larger number of patients with metabolic disorders. Amylin analog drugs are gaining popularity because they help regulate blood sugar levels while also reducing appetite and supporting weight management.

Another major factor driving market growth is the increasing demand for combination therapies. Many conventional diabetes treatments contribute to weight gain, while amylin analogs offer a more favorable metabolic profile by enhancing satiety and improving glucose control. Combination therapies involving amylin analogs and GLP-1 receptor agonists, such as CagriSema, are demonstrating stronger weight-loss outcomes compared to GLP-1 monotherapy alone.

The market is also benefiting from the development of long-acting formulations and patient-friendly drug delivery systems. Pharmaceutical companies are focusing on once-weekly and once-monthly injectable therapies, as well as disposable injection pens that improve convenience and adherence.

Why Is Pramlintide Dominating the Amylin Analog Drugs Market?

Pramlintide dominated the market with a 55% share in 2025 because it remains the most established and widely prescribed amylin analog for patients with type 1 and type 2 diabetes. It is currently the only amylin analog approved by the U.S. Food and Drug Administration and has a strong track record in improving post-meal glucose control, slowing gastric emptying, and promoting satiety.

The ipragliflozin segment held the second-largest market share of 35% in 2025 and is expected to grow at the fastest CAGR of 9% during the forecast period. Its growing use in diabetes management is driven by its ability to enhance insulin sensitivity, reduce postprandial glucose levels, and support urinary glucose excretion.

What Opportunities Are Emerging from Combination Therapies and Next-Generation Peptides?

Combination therapies are creating some of the most attractive opportunities in the amylin analog drugs market. Pharmaceutical companies are increasingly exploring combinations of amylin analogs with GLP-1 receptor agonists and GIP agonists to create more effective metabolic treatments. These therapies are designed to improve satiety, reduce appetite, and achieve stronger weight-loss outcomes.

Another major opportunity lies in the development of dual amylin and calcitonin receptor agonists, as well as triple agonists such as retatrutide. These next-generation therapies are being designed to deliver broader metabolic benefits, improved insulin sensitivity, and better obesity management. Community discussions also show rising interest in therapies such as amycretin, cagrilintide, and eloralintide because they offer longer-lasting effects and stronger weight reduction than traditional therapies.

Which Segments Are Leading the Amylin Analog Drugs Market?

The pramlintide segment led the market with a 55% share in 2025, followed by ipragliflozin at 35%. Other amylin analog drugs accounted for 10% of the market. Subcutaneous injection dominated the route of administration segment with an 80% share because it provides strong bioavailability, reliable dosing, and ease of use. Intravenous injection represented 20% of the market and is expected to grow at a CAGR of 8.2% because of its increasing use in hospitals and acute care settings.

The type 1 diabetes segment held the largest market share of 50% in 2025 because patients with type 1 diabetes do not naturally produce amylin and therefore benefit significantly from replacement therapy. Type 2 diabetes accounted for 40% of the market and is expected to grow at a CAGR of 8.5% during the forecast period because of the rapidly expanding diabetic population. Meanwhile, the obesity segment is expected to grow at the fastest CAGR of 9% due to increasing demand for satiety-based weight management therapies.

Why Do Hospitals Lead the Market?

Hospitals dominated the amylin analog drugs market with a 60% share in 2025 because these therapies require specialized storage, administration, and monitoring. Hospitals are better equipped to manage insulin therapy, glucose monitoring, and injectable medications that require cold-chain logistics and professional supervision.

Clinics held the second-largest market share at 25% in 2025 and are expected to grow at a CAGR of 8% because they provide outpatient metabolic care and personalized patient education. Homecare settings accounted for 10% of the market and are expected to grow at a CAGR of 8.5% because telemedicine, remote glucose monitoring, and self-administered injectables are becoming more common.

Why Is North America Dominating the Global Market?

North America held a 40% share of the global amylin analog drugs market in 2025 because of its high prevalence of obesity and diabetes, well-developed healthcare infrastructure, and strong reimbursement environment. The region has a large patient population requiring advanced metabolic therapies and a healthcare system that is capable of supporting specialized injectable treatments.

The United States remains the largest country-level market because nearly 40% of the adult population is obese and approximately 38.4 million people were living with diabetes in 2024. These factors are creating substantial demand for therapies that support glycemic control and weight management. Europe held the second-largest share in 2025, while Asia Pacific is expected to witness the fastest growth due to rising healthcare expenditure, increasing metabolic disease prevalence, and expanding pharmaceutical manufacturing capabilities.

What Are the Latest Breakthroughs and Innovations in the Market?

Manufacturers are increasingly focusing on long-acting amylin analogs, once-weekly injectables, dual receptor agonists, and patient-friendly delivery systems. These innovations are helping improve treatment adherence and deliver stronger weight-loss and glycemic control outcomes. The market is also witnessing increased use of disposable injection pens and combination therapies that improve convenience and ease of use.

Case Study: CagriSema Highlights the Future of Combination Therapy

Combination therapies are becoming one of the most promising strategies in metabolic care. CagriSema, a combination of cagrilintide and semaglutide, has demonstrated stronger weight-loss outcomes compared to GLP-1 monotherapy alone. Market observers believe that these combination therapies could redefine obesity treatment and expand the role of amylin analogs beyond diabetes management.

Get Sample Link: https://www.precedenceresearch.com/sample/8317

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at sales@precedenceresearch.com